Singapore’s Housing Market Just Took a Chill Note

In a move that feels a little like a neighborhood cooldown blanket, the Singapore government pushed through a series of measures aimed at taming the housing market. The effect? Fresh new listings and resale prices giving a little nudge downwards. That’s good news for folks who’re ready to dive into buying their first home.

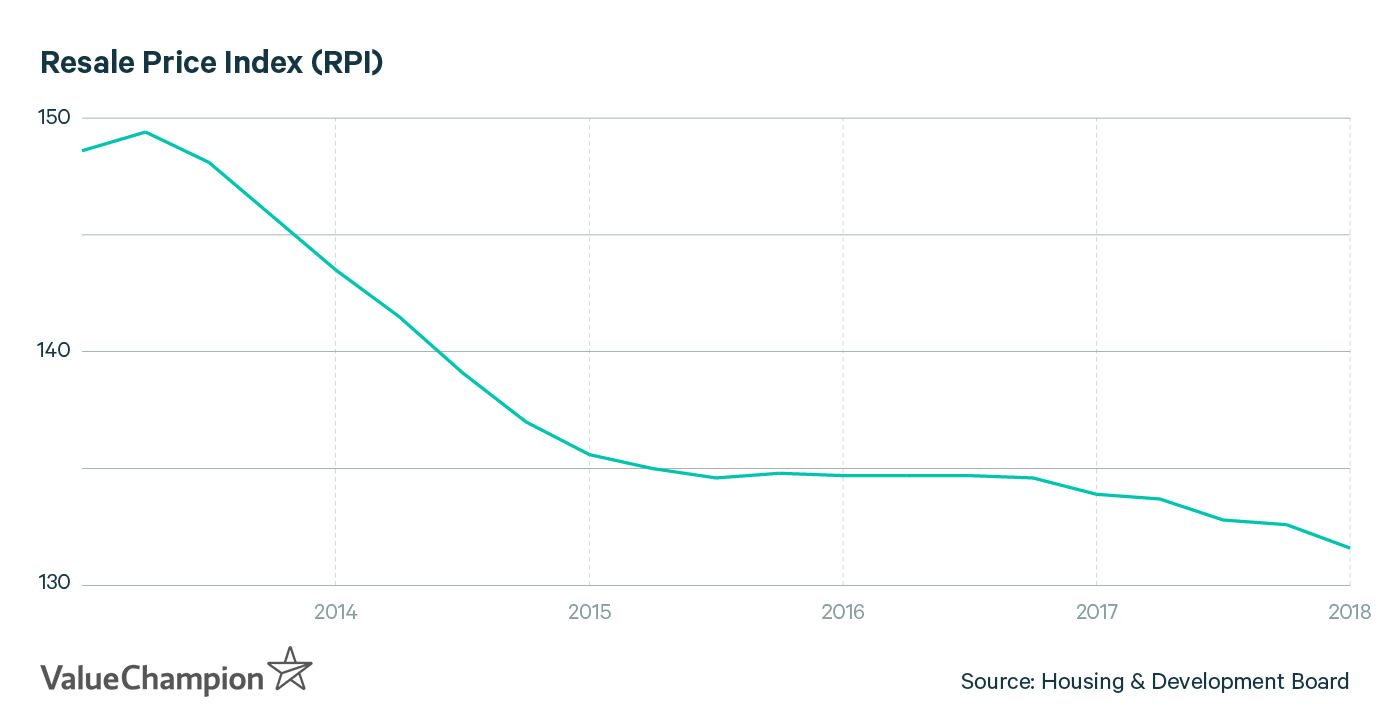

What the Numbers Are Telling Us

- HDB Resale Price Index: Down by 2 points compared to a year ago.

- Private Non‑Landed Homes: Fell for the first time in 8 years—since 2018—in August.

These figures are definitely a breath of fresh air for the price‑hungry crowd. Still, before you put on your “I’m ready to buy my first home” jersey, consider the bigger picture.

Beyond the Price: What to Check Out

- Interest Rates: Even modest changes can shift monthly repayments. Locked‑in rates today might offer instant relief, but are they still competitive tomorrow?

- Loan Approval Criteria: Your credit score, income, and even the landlord’s history can affect your loan. It pays to review these before you chase the perfect property.

- Future Market Outlook: Prices aren’t forever flat. Economic indicators, housing supply, and government policy changes can throw a curveball.

- Location Amenities: Proximity to schools, hospitals, and offices can swing the resale value in the long run—so don’t just chase the detective of the lowest price.

- Lifestyle Fit: Assess whether the neighbourhood vibes align with your everyday life—late‑night food spots, park access, and even the noise level.

What This Means for You

If you’re itching to get into the property game, remember these points like a checklist. Think of it as stressing from all angles: price, financing, future trends, neighborhood feel, and the overall “you’ll still love it when you’re old.” A smart buyer checks all boxes before making an offer.

Bottom Line

Singapore’s housing prices might be cooling, but enthusiasm for jumping in remains high. If you plan wisely and look beyond just the price tag—consider rates, future context, and the place’s vibe—you’ll find a spot that feels forever right.

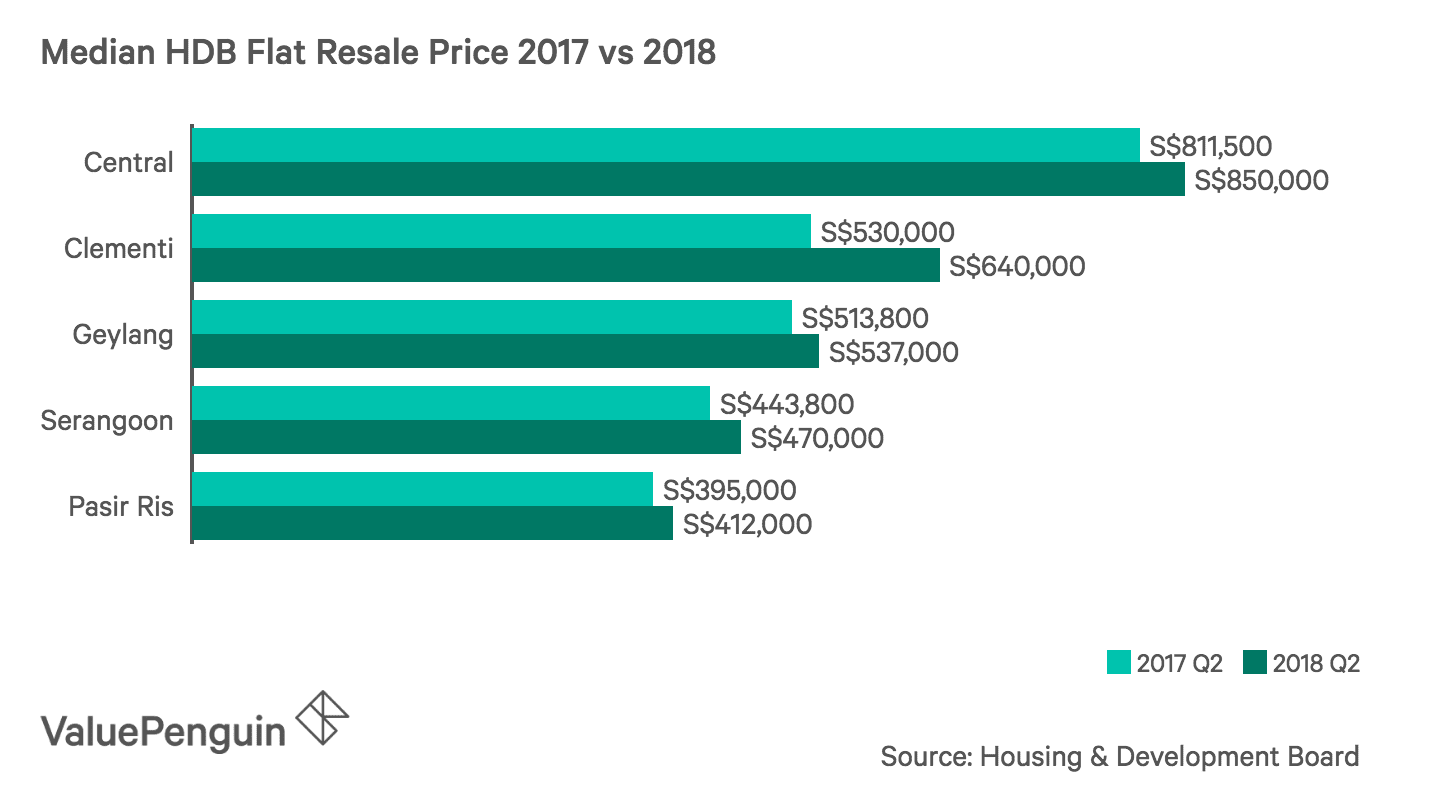

When Some Singapore Streets Get Pricier

Sure, the overall market trend is a bit down‑beat, but that’s not the whole story. Grab your glasses – some neighborhoods are actually charging more this year.

Spotlight on the Gains

- 21% hike in the median price of a 4‑room HDB flat in Clementi. That’s more than the price jump of a dragonfly per dollar!

- Serangoon, Central, and Geylang each brag about a +5% increase. Not a trivial bump, but a definite eye‑catcher.

Why It Matters

Don’t be fooled by the average drop. If you’re eyeing a neighborhood, dig a little deeper. Knowing the price trend in your sweet spot will keep you from falling ill‑prepared when you’re asking your bank for that down‑payment. Plan, save, and then watch those numbers on the dream home stack rise – the way you want them to.

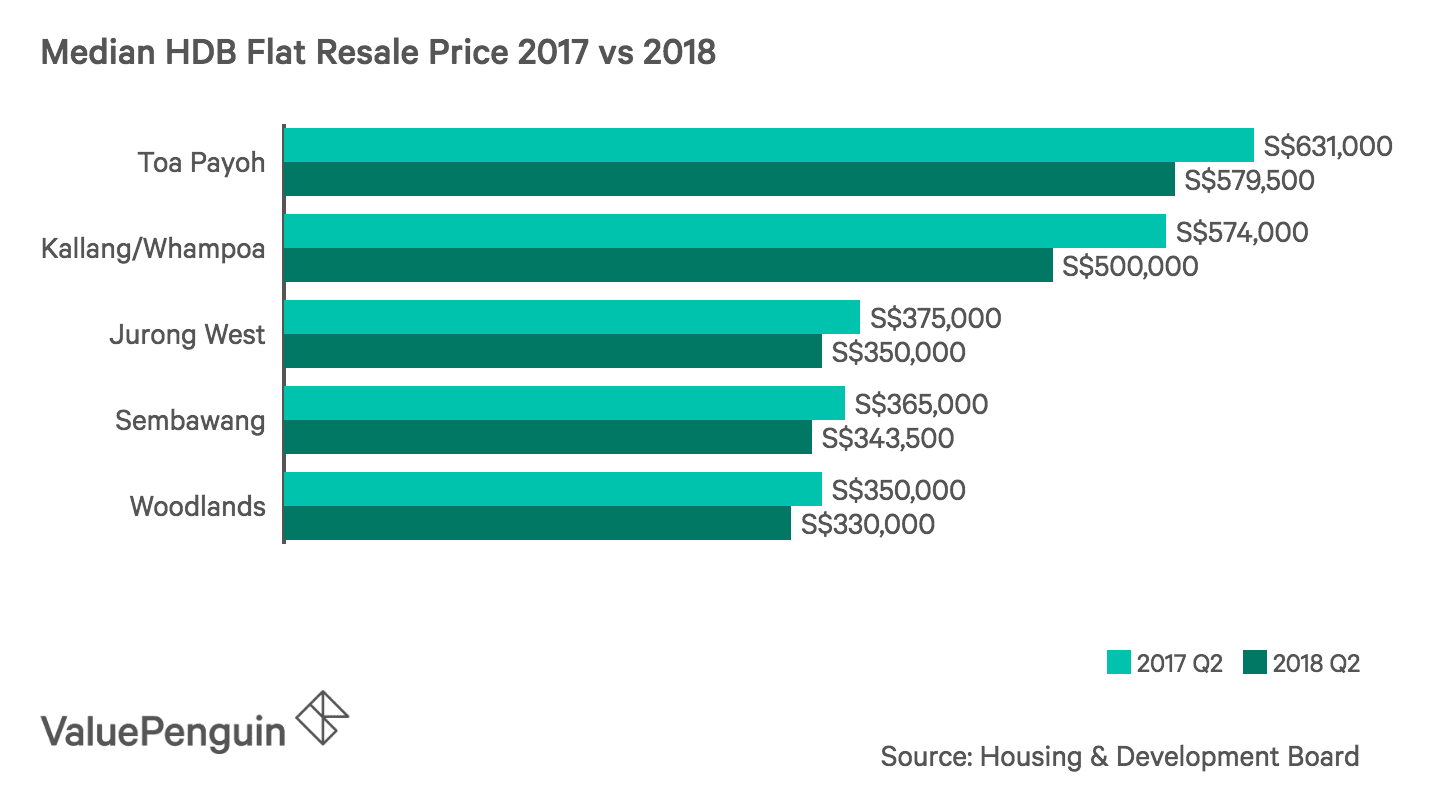

Good News for First‑Time Homebuyers

Feeling the pinch when you’re on the hunt for your first house? Take a breath – there’s a bright side. Over the last year, many Singapore neighbourhoods have seen a sharp drop in property prices.

Where the bargains are hiding

- Kallang/Whampoa – 13% off the median price of 4‑room HDB flats

- Woodlands – 6%–8% reduction

- Sembawang – 6%–8% reduction

- Jurong West – 6%–8% reduction

- Toa Payoh – 6%–8% reduction

So, if you’re in the market for a place that won’t break the bank, these areas should be on your shortlist.

Why it matters

Price dips like these mean more budget to play with, whether you want to splurge on kitchen fittings, invest in a nice view, or simply save for those sweet future adventures.

Next steps

1. Do your homework: Check current listings, compare prices, and factor in local amenities.

Now that your wallet’s got a little breathing room, the thrill of getting a home starts to feel less like a distant dream and more like a reality you can reach!

Home Prices in Singapore: Not All Low, All Yours

The city’s average house cost is on a downward slide, but that’s not the whole picture. Different districts are charting their own stories—some are doing fine, others are still holding their ground.

Before You Commit, Do Your Homework

- Scan the recent sales data for the neighborhoods you’re eyeing.

- Check whether those plots have had a price drop or are holding steady.

- Don’t leap straight into a deal; a little research can save you a bundle.

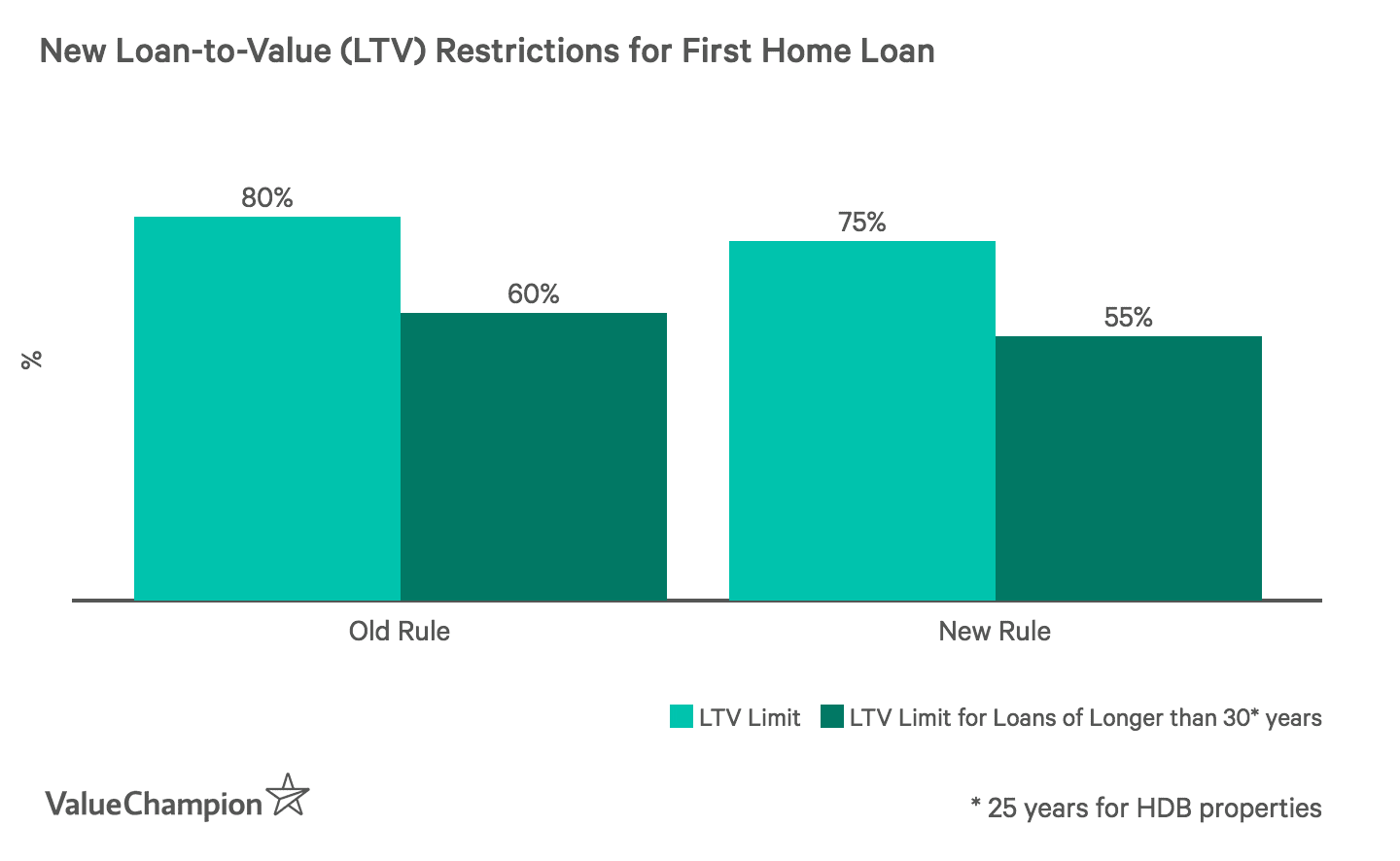

Rules That Can Make or Break Your Dream

It’s not just the price tag that matters. The government’s rules can tip the scales.

New Loan‑to‑Value Limits for First‑Time Buyers

In July, the Ministry tightened the Loan-to-Value (LTV) rules. Now, most first‑home loans need a down‑payment of 25%:

- Minimum 5% cash. That’s the immediate upfront bite.

- The remaining 20% can come from your CPF Ordinary Account.

Why does this matter? Because knowing this split tells you roughly how much you need to stash away before you can sign the contract.

Bottom Line

Keep your eye on the trends, ask the right questions, and you’ll avoid stepping into a price‑sick or rule‑tight spot.

What’s the Real Deal with Home‑Buying Costs?

Buying your first house isn’t just a celebration; it’s a math puzzle that involves a few sneaky numbers you’ll want to know before you hand over your money. Below we break down the main players in this cost game—Sum it all up, and you’ll see why the sweat‑pants-and-couches mentality hardly applies to the mortgage world.

TDSR: The Debt‑Pay‑Rate Gatekeeper

First off, the Total Debt Servicing Ratio (TDSR) is like the financial version of a “no‑entry” sign for your loan office.

It caps the total monthly debt you can have (home loan, student loan, credit card) so it doesn’t exceed 60 % of your income. In practice, you simply take 60 % of whatever you earn each month, then slap out all other debt obligations, and what’s left is the ceiling for your mortgage payment.

For a first‑timer, this rule is crucial because you’ll likely rely almost entirely on a loan to get behind the doorstep of your dream home.

How Much Does Owning a Home Actually Cost?

The price tag you see on the house isn’t the full picture. Think of it as buying a fancy burger plus all the extra toppings that show up on your bill later. Here’s a quick rundown of the extra costs to watch out for:

Mortgage Payments

Everybody knows you need a down‑payment, but the rest of the story is about that monthly mortgage. The more cash you can throw down up front, the smaller each monthly slice will be, and over time the total interest you’ll pay shrinks too. Use a home‑loan calculator to see how different rates or down‑payment sizes change your monthly bills.

Utilities

“Isn’t electricity, gas and water that’s just a few bills? Isn’t that it?” Think again. In Singapore, the average home spends about S$150 a month—that’s S$1,800 a year. It may look innocuous, but it’s real cash outflow you have to add to your budget.

Home Insurance

There’s always a chance something goes wrong—storms, accidents, or just that one stubborn toaster that decided to ignite. A standard policy for a 4‑room HDB flat can be around S$154 a year, but deals like NTUC Income’s offer S$51 per month. Take the time to compare plans; a cheaper policy may still leave you exposed to bigger risks.

Key Takeaways for First‑Time Buyers

- Budget beyond the sticker price: Remember mortgage, utilities, and insurance add up.

- Know your TDSR limits: It’s the upper bound on what your loan can be. Don’t assume you can borrow more than your income allows.

- Build a realistic financial picture: Add down‑payment, monthly payments, utilities, and insurance into one tidy spreadsheet.

- Be honest with yourself: If the total costs feel like a ballpark hit for an athlete but you’re a beginner, maybe hold off until you feel more financially solid.

- Read the fine print: Whether it’s interest rates or insurance terms, the small lines can sway your monthly budget.

When the house prices look like they’re dropping, it may feel like a golden ticket; yet make sure you’re truly ready to jump into the homeowner’s club. The best move is to crunch the numbers and see if your personal financial situation clears the doorway.

— This was originally shared by ValueChampion in the Property section, designed to keep you informed and ready for the real cost of homeownership.