Turning 35? Time to Grab That One‑Bedroom Dream!

Woke up, checked the usual feeds, hit like on your friends’ #anniversary and #babyturnsONE pics, and realised something: today is your 35th birthday. Congrats! That means the Government’s finally handing you the ultimate consolation prize – a flat for you.

What the HDB has in Store for Solo Stars

The Singapore housing system now offers two sweet spots for single citizens: the Singles Singapore Citizen scheme and the Joint Singles Scheme. Both let you pick new or resale units, but the rules differ a smidge.

- BTO (Build‑To‑Order): you’re limited to 2‑room Flexi units in non‑mature estates. Think less apartment drama and more single-room vibes.

- Resale: No ceiling on size or location. If you fancy a 3‑room, a 4‑room, or even a studio that’s on the same street as your neighbours, it’s all fair game.

Quick Eligibility Snapshot

Just like a treasure hunt – clues and a prize. Here’s the pit stop checklist:

- ⏰ Age Criteria: Must be between 35 and 60 years old.

- No Marriage: You’re single; no partner, no co‑applicants.

- Financial Suitability: You need to demonstrate enough income or savings – think of it as your “home‑buying payslip.”

- Postage of Ownership: The flat will be solely in your name – no rocking or trembling tenants on the same account.

Next Steps: From Gifs to Guts

Grab a cup of kopi, pour your heart into that application form, and remember: the ultimate flogging of disappointment turns into a fine ?

Let’s toast to new doors, fresh tiles, and a fresh start at 35. Cheers to yourself, the only co‑owner you need!

Flat‑Buying Rules for Singapore Residents

Picture this: if you’re a Singapore citizen, you’re allowed to snatch up a flat, but only once you hit the right age. If you’re flying solo, you’re looking at the 35‑year‑old milestone—unless you’re a widow or mother of a young orphan, then the clock starts ticking at 21.

Who’s in the Game

- Singles Singapore Citizen – for lone saints who want to own a place on their own.

- Joint Singles Scheme – a buddy‑system where 2 to 4 single citizens can pool together. Everyone has to meet the same age trickery, and you all have to show up as co‑applicants.

Once you’ve Met the Age Threshold

Now you can pick whether you want a brand‑new Build‑To‑Order (BTO) home or you’re eye‑ing a resale property. Both have extra hoops to jump through, but don’t worry—those details are coming up next.

Ready to Grab an HDB Flat?

Thinking about snagging a brand‑new BTO or a resale gem? Here’s the low‑down on who gets what, how much you can afford, and the handy grants that can give your savings a boost.

Income Rules – What’s the Cut‑off?

- BTOs: The income ceiling is $6,000 per month. If you’re farming you can still apply but no more than that.

- Resale for Singles: No income ceiling, but CPF Housing Grants and HDB Loans come with their own max‑income limits.

Grab the Grants – 4 Flavor Options

Happy to help you keep more money in your pocket! Four grant types are on the menu, all of which land straight into your CPF Ordinary Account:

- Additional Housing Grant (AHG)

- Special Housing Grant (SHG)

- Enhanced CPF Housing Grant – Singles Grant

- Proximity Housing Grant

What do they do?

- They offset the purchase price of your flat.

- They reduce the mortgage loan you need to take out.

- Watch out: you can’t use them for down‑payment or monthly mortgage bills.

For Singles: 2‑Room Flexi BTOs

Got your eye on a fresh 2‑room flexi BTO? Check if your profile matches the eligibility criteria before you lock in the deal.

Should You Apply?

- If your income is ≤ $6k and you’re looking at a BTO.

- If you’ve got a resale option and want that extra boost from CPF grants.

- Remember: a trial run with the eligibility screener can save you a tonne of time and frustration.

Good luck hunting your future home—let the grants do most of the heavy lifting!

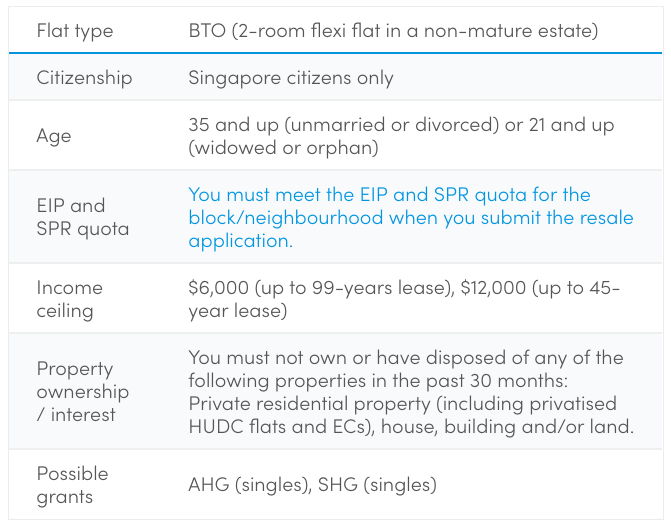

New HDB Flat Hurdles – What You Need to Know

Ready to snag an HDB gem? First off, keep the numbers in check: the income ceiling sits at $6,000 for a 99‑year lease and doubles to $12,000 for a 45‑year lease. If you’re blowing through the budget line, you’re out of luck.

What’s on Offer?

Only 2‑Room Flexi in Spiky New Estates

- Type: 2‑room Flexi

- Where: Non‑mature estates (≤20 years old) – think Bukit Batok, Sembawang, Punggol.

- Size: 36 sqm (Type 1) or 45 sqm (Type 2)

- Layout: One bedroom, one bathroom, a kitchen, a storage space or a tiny “shelter” portion.

In plain English, these units are the definition of “cosy” – if you’re having a mini‑vacation in a 36‑sqm room, expect a hotel‑style flat power draw. For the grandiosely spacious, you’ll have to look at resale units instead.

Need a Bare‑Bones Crib?

While a tight, 36‑sqm Flexi unit might be perfect for a bachelor or the newest single, any extra space ambition? We’ve got resale options up our sleeve, and if you’re planning a future partnership, consider going small first. Then, after a few years, you can re‑apply for a BTO as a “first‑timer” couples – a neat trick for growing families.

What About Your Other Property?

Already owning a private house? No worries – you’re still eligible to join HDB’s BTO or resale market. The catch: you must let go of that other property at least 30 months before submitting your HDB application. The idea is simple: HDB expects you to live in the flat, not just sandbox it in your investment portfolio.

CPF Housing Grants – The Pyramid of Relief

When you’re ready to dive into the HDB pool, you’ll have a few handy CPF grants to smooth the way:

- Agricultural Household Grant (AHG) – a sweet perk for low‑to‑mid‑income families.

- Subsidised Housing Grant (SHG) – the big money saver for most households, covering a significant chunk of the construction cost.

So, you’ve got the rules, the choices, and the lifeline grants. Get your ducks in a row, keep those income numbers tidy, and you’ll be living your best Singaporean dream in no time!

Grab the Extra Grant – No, It’s Not a Lottery Ticket!

Welcome to the world of CPF housing grants, where $20,000 can kickstart your home‑buying journey, but only if you’re locked down at a $2,500/month income ceiling.

What’s the Deal with the Additional CPF Housing Grant (AHG)?

- Maximum Value: Up to $20,000 – no matter if you’re buying a resale or a new BTO unit.

- Income Cap: Your gross monthly income must stay at or below $2,500. Think of it as a “salary freeze” that pays for your home instead.

Double Trouble? Or Double the Grant?

The Special CPF Housing Grant is your second chance. It’s only for BTO orders, but it raises the income ceiling to $4,250/month. If you meet the conditions, you can stack both grants to get a sweet combo of subsidies.

- Eligibility: Same BTO purchase, but your paycheck can be a little fatter.

- Stacking Bonus: Work the two grants together – your down‑payment could feel like a holiday gift.

Need exact numbers, fine print, or a quick “is my salary okay?” check?

Head on over to the HDB official website. They’ve got all the details posted there, so you don’t have to guess what “eligible” really means.

Singles & Resale – Nothing Novel Here

If you’re signed up for a brand‑new flat and your monthly income exceeds $6,000, the verdict is: you’re out of luck for the new build. But don’t stress – the resale market is still open for you to swing by.

So grab your calculator, check your figures, and get that house‑buying plan approved. Note: having a higher income isn’t a death sentence – you just need to navigate the resale market. Happy house hunting!

Buying an HDB Resale Flat: What You Need to Know

Good newsheads! If you’re single and dreaming of owning an HDB flat from the resale market, the biggest hurdle—an income ceiling—doesn’t exist.

Income Limits Sweet Spot

- No income cap for simply buying a resale flat.

- But if you’re eyeing CPF Housing Grants or an HDB loan, there is a maximum income limit.

- In plain speak: If you can comfortably pay off the flat before you hit 35, you’ll skip the extra help.

Freedom of Choice on Flat Types

Resale? That’s one small word with big perks. Unlike BTOs, you can pick any location and size:

- Why not a 5‑room beauty in Bishan if the price tag is in your lane?

- No geographic or size restrictions.

Ownership Rules — Quick & Easy

There’s a simple rule about owning another property:

- Before you apply, you must sell any prior property.

- Resale does only require you to have done this at least 6 months before application.

- That’s 24 months “lighter” than the rule for BTOs.

CPF Housing Grants for Singles

You can grab:

- Singles Grant

- Additional Housing Grant (AHG)

- Public Housing Grant (PHG)

Each grant can lighten the financial load, so check which one applies to your situation.

All in all, buying a resale HDB flat is a breeze. No income ceiling, endless choice in size and location, a relaxed ownership rule, and some handy grants can make the dream a reality.

Mind the Money While Buying a Singapore HDB Home

Got the idea of snagging a new BTO or a resale flat? The Housing & Development Board (HDB) is rolling out grants that could help you get a decent chunk of the bill paid. Below you’ll find the scoop on the goodies available to single applicants and a quick checklist before you jump in.

Grant Highlights for Singles

- Singles Grant – If you’re buying a 4‑room or smaller resale, you can pocket an extra $25,000. For 5‑room flats it’s $20,000. The eligibility ceiling? Up to $6,000 in monthly income per single applicant.

- Proximity Housing Grant – Living close to your parents (within 4 km) earns you another $10,000. Paperwork’s straightforward; just proof the distance.

- Resales bring you extra CPF grants – but they’re less generous than the singles grant. Check the official HDB site for the exact numbers and conditions.

Four Things to Think About Before Signing the Papers

- Future Income Growth – Turning 35 is a milestone. If you wait, your salary might push you over the $6,000 threshold, and you’ll lose eligibility for both the BTO grant and the singles grant. Don’t let the lottery of salary bumps sneak up on you.

- Real Affordability Check – Grants look great, but your TDSR (Total Debt Servicing Ratio) matters. Pretend your income is low to squeeze in extra subsidies, but don’t smuggle it around; banks see through that. Also, remember that the down‑payment is just the tip of the iceberg—renovations, moving costs, and the extra charges of owning a new place can add up fast.

- Moving Away From Parental Comfort – If you’ve been living under your parents’ roof, you’ve got a cushion of existing utilities and perhaps a more mature neighbourhood. A fresh flat means new rent, new utilities, new maintenance, and the same 2‑room setup you already know. Budget those extra living costs before you make the move.

- Do You Plan to Marry? – 3 to 5 years to get the keys, plus a 5‑year Minimum Occupation Period (MOP). That’s 8 to 10 years before you can actually leave that 2‑room slice of the city. If marriage is in the cards and you both have big dreams of a bigger house once a partner is found, you might want to hold off and target a resale unit that aligns with future partner perks or a larger BTO with a deviation for larger units if you qualify.

Need the nitty‑gritty grant numbers? Always ping the HDB website for the most up‑to‑date rules and figures. And remember: These grant policies are like pop‑corn—once they’re out, they’re not going back in. So take a gander, weigh your options, and don’t stall the home‑owning adventure if the numbers are in your favour.