Singapore Savings Bonds: A Friendly, No‑Boring Guide

Ever wondered how to let your money grow without risking a break‑neck ride? Singapore Savings Bonds (SSB) are the crowd‑pleaser. They usually give a higher return than the old‑school bank fixed deposits, and they’re the go‑to for risk‑averse folks looking to keep up with Singapore’s steady 2.5% inflation since 1962.

Why SSB Are a Smart Pick

- Liquidity – you can pull your cash out whenever you need it.

- Ease of Entry – a quick online application is all you need.

- Always Improving Rates – in recent months the rates have nudged up slowly, keeping your money a tad more competitive.

SSB vs. Regular Bank Savings – The Quick Take

- Availability – both are fairly easy to get into.

- Return Rates – SSB can sometimes outpace a typical savings account (which often sits below 1%).

- Flexibility – you can withdraw from both, but having your money stuck in a savings account has no sweat.

SSB vs. Fixed Deposits – The Straight‑Up Comparison

- Liquidity – SSB allows full withdrawals on demand; Fixed Deposits sometimes slash your earnings with penalties.

- Getting Started – both are a breeze; just launch a fast online application.

- Returns Over 1%? – SSB can exceed 1% in certain years, while Fixed Deposits usually hug a low‑hundreds‑thousandths-per‑cent rate (around 0.05% baseline).

In short, if you’re watching inflation, want easy cash flow, and like seeing your savings do a little workout, SSB is your ticket. But if you’re a “lock‑in” fan who loves that extra bit of security, a fixed deposit still has its own charm. Happy investing!

TL;DR: This month’s Singapore Savings Bonds (SSB) interest rates

Why the SSB Interest Rate Wavers Every Month

Every month, the SSB interest rate takes a spin, almost like a roulette wheel that never quite goes to the same spot. If you thought the markets were already a circus, the SSB’s behaviour is just the grand finale. Here’s why you should buckle up and enjoy the ride.

1. The Pulse of the Economy

- Inflation whispers: When prices start climbing, the central bank jolts up the rate to keep the currency steady.

- Employment chatter: Booming job numbers can push rates higher; a sluggish job market might pull them back.

- Global vibes: Economic signals from abroad—think trade talks, sanctions, or geopolitical drama—send ripples that the SSB feels.

2. The Policy Makers’ Dance

Every meeting, a group of economists scribbles ideas on whiteboards. Their decisions are often a mix of rational math and a dash of instinct. At the end of the day, they are humans who care about growth, stability, and that good old feel of a thriving market.

3. The “Easter Egg” Factor

- Unexpected events: A surprise election, a climate crisis, or a sudden tech breakthrough can shift the SSB’s outlook.

- Market reaction: Traders, investors, and savers might spin the rate around as they adjust portfolios.

- Humor break: Even seasoned economists occasionally say, “Let’s keep tickling that rate!” just to keep the atmosphere light.

4. Why You Should Care (and How to Stay Updated)

If the SSB rate goes up, you’ll pay a bit more on home loans and credit cards, but you’ll also earn more on savings. When it dips, borrowing costs ease, but your savings bank account might feel a bit lighter. Stay on top by reading the official releases—or, if you’re fancy, subscribe to newsletters that translate the jargon into plain English.

5. A Quick Summary

SSB’s monthly rate changes track the economy’s health, the policy makers’ judgments, and a few surprise global events. Think of it as a constant balancing act—sometimes you get a slight tilt, sometimes a full twist. The key is to stay informed and lean into the financial world’s ever-shifting dance.

Singapore Savings Bonds for January 2022

What You Need to Know

- Bond ID:

GX22010S– Watch for this code in your CDP (labeled SBJAN22) and in your SRS statement. - Issue Date: 3 January 2022

- Maturity: 1 January 2032 – A decade of reliable returns.

The Application Countdown

Set your alarms! The window to book this bond opened on 1 December 2021 at 6 pm and closed on 28 December 2021 at 9 pm.

- Allotment: 29 December 2021, after 3 pm – Your bond will be allocated and you’ll get the confirmation.

- Issuance: 3 January 2022, end of day – That’s when the bond officially enters your portfolio.

When You Can Redeem

The redemption window matches the application window: 1 December 2021, 6 pm to 28 December 2021, 9 pm.

- Redemption Date: 3 January 2022, end of day – Just in case you decide to pull out.

Happy saving! Keep an eye on these dates, and you’ll make the most of your Singapore Savings Bonds.

Singapore Savings Bonds (SSB) interest rates

What’s the Deal with This Month’s Singapore Savings Bonds?

Let’s dive into the numbers in plain English—no fancy jargon or hidden math. It boils down to: how much you’ll likely earn if you lock your cash into a Savings Bond for a set number of years.

Year‑by‑Year Snapshot

| Years Held | Annual Rate (percent) | Average Return (percent)* |

|---|---|---|

| 1 | 0.41 | 0.41 |

| 2 | 0.95 | 0.68 |

| 3 | 1.24 | 0.86 |

| 4 | 1.48 | 1.02 |

| 5 | 1.71 | 1.15 |

| 6 | 1.94 | 1.28 |

| 7 | 2.11 | 1.39 |

| 8 | 2.29 | 1.50 |

| 9 | 2.51 | 1.60 |

| 10 | 2.78 | 1.71 |

*These averages are calculated on a compound basis at the end of each year.

What Happens If I Invest $1,000?

Picture this: you stash $1,000 in a 10‑year Savings Bond. You’ll be ringing a bell in just 10 years—actually, a $180 interest bonus, roughly a 1.78% effective yearly return. Not too shabby for a bank‑safe, low‑risk investment, right?

Why It’s Worth Checking Out

- Interest rates climb gradually, so the longer you stay, the more you earn.

- Enjoy a predictable return with no nasty surprises—missing a payment is just a bit of hassle.

- Good for folks who want to build a financial cushion without the volatility of stocks.

That’s the lowdown! Give it a quick look if you’re planning to lock in some financial sweet‑spot for the next decade.

What is a Singapore Savings Bond?

A Friendly Introduction to Singapore Savings Bonds

Let’s dive into the world of Singapore Savings Bonds (SSBs)—the government’s own passport to a secure and flexible long‑term savings adventure. In plain English, SSBs are a simple, low‑risk way for you to park your money and let it grow over time, all while enjoying a bit of fiscal flexibility.

Why the Government Loves SSBs

- Safety First: The Singapore Government backs them, so you can sleep well at night knowing your funds are protected.

- Flexibility at Your Fingertips: Want to tap into your savings before the bond matures? No problem—partial redemptions are allowed.

- Long‑Term Growth: Designed for the big picture, these bonds help your money compound over several years.

Who’s the Ideal SSB Fan?

Whether you’re a meticulous planner, a future house‑buyer, or just someone who likes to avoid the roller‑coaster of the market, SSBs fit neatly into that routine. They’re especially great for:

- Students saving for university,

- Families preparing for a future home,

- Anyone who appreciates low‑risk, crowd‑sourced growth.

A Touch of Humor

If you’ve ever wished your savings had a safety blanket, think of SSBs as that blanket wrapped around a cozy, long‑lasting blanket of investment. They’re the economic equivalent of a good friend who says, “I’ve got your back, no matter how long it takes.”

Final Thoughts

In short, Singapore Savings Bonds are your friendly, government‑guaranteed partner that offers safety, flexibility, and a steady chase of your long‑term financial goals. Grab one today, and watch your money grow while you keep calm and carry on.

What are the benefits of parking my savings with SSB?

Investing in SSBs: What the Buzz Really Means

Why We’re Talking About SSBs

Think of an SSB like a secret menu item at your favorite coffee shop—spicy, flavorful, but you’ve gotta know the risks before you order. It’s all about striking that sweet spot between growth potential and risk tolerance.

Benefits Everyone’s Whispering About

- Steady Returns: Even in shaky markets, SSBs often keep their heads calm, offering a gradual yet consistent rise.

- Tax Perks: Some SSBs come with tax‑friendly bonuses, making your portfolio feel like a pig‑squeak of savings.

- Fresh Opportunities: They often back innovative ventures, giving you a front seat to the next big thing.

- Management Team: Leaders with track records—think you’re getting the probers most investors crave.

Risks That Might Pop Your Bubble

- Liquidity Concerns: Some SSBs are like obscure indie albums—they’re hard to sell quickly if you need cash.

- Market Volatility: While they’re usually stable, the market can still swing like a yo‑yo, especially during economic turbulence.

- Regulatory Hurdles: Changing rules could throttle the growth of your SSB, like a surprise rainstorm on your lawn.

- Early Losses: Small-scale ventures can sometimes misfire, leading to early disappointments that cost more than they make.

Bottom Line—Should You Jump In?

It boils down to your appetite for careful optimism versus bold ambition. If you’re ready to dwell on the little victories but keep an eye on the big risks, an SSB might be just the right addition to your portfolio. If the thought of a sudden drop in value makes you swoop your knees, you might want to hold back until the market screams a little more confidence.

1. No penalty for early redemption

Saying “See‑You” to the Bank’s Head‑Hold Free

Got a dollar (or a few) that keeps getting stuck in a bank’s “I’m holding it for you” fence?

With the SSB, the longer you let it sit, the sweeter the interest you’ll get—plus there’s zero fine if you decide to pull it out early.

What Happens When You Pull Your Money

Just submit a redemption request and you’ll be paid back the principal plus any earned interest by the 2nd business day of the next month.

- January redemption of $1,000: You receive your $1,000 and all the interest by the 2nd business day of February.

- No “holding cost” penalties—so you can skip the long‑term lock‑up and still keep the reward.

Why This Might Be a Good Idea

If the thought of your money being on hold for months makes you sweat, the SSB offers a flexible alternative. It’s like having a car that pays you if you keep it parked in a spot for a while—only this time, it’s your money you get the benefit for.

2. Fully backed by the Singapore government

Why the Singapore Savings Bond (SSB) is Basically Money‑Made‑of‑Gold

Picture this: you put your hard‑earned cash into the SSB, and you’re basically getting a “golden ticket” from the Singapore government itself. No matter if you’re a fan of politics or not, the Fact is that the Singapore administration is riding on a AAA credit rating. Yep, that’s top‑notch, sky‑high trust.

Reduces Risk to Almost Zero

Need to keep your money safe? The SSB levels the playing field. The AAA rating slashes the risk down to almost nothing—though, like all investments, a kink or two can still pop up.

Only a Few of the Elite Get This Tag

It’s not just Singapore that has that shiny star. Nations like Switzerland and Hong Kong float with the same AAA badge too. These are the “few and far between” kinds of countries where the financial drama is basically a whispered lullaby.

Bottom Line: The SSB is One of the Safest Bets in the Market

Because Singapore’s credit rating is rock‑solid, the SSB practically reads “this is a safe, steady, super‑smooth deal.” So if you’re after the gold‑standard of security, this bond is basically the gold standard. Invest confidently, and let the Singapore government keep your money smiling.

3. $500 is all it takes

Investing in SSBs Made Easy (No Need to Run on Grass)

Good news for the budget‑savvy and the high‑rollers alike!

The Minimum Entry Fee

You only need to drop $500 into the system—yes, that’s a tidy sum, not a fortune.

That means almost everyone can start tossing their pennies into SSBs without the drama of binge‑shopping or taking up a competitive goat‑herding hobby.

But There’s a Ceiling

The individual limit per SSB is capped at $200,000. That figure includes:

- Bonds you buy outright with cash.

- Funds coming in from your SRS accounts.

So even if you’re a millionaire, you can’t just pour all your wealth into a single SSB. It’s like being told to stop buying avocado toast—no matter how much money you have!

Bottom Line

SSBs are a flexible, accessible option: low minimums, a clear upper bound, and a rule that keeps the game fair for everyone.

Step-by-step guide to investing in your first Singapore Savings Bonds (SSB)

How to Apply for Singapore Savings Bonds

Step 1: Check Your Eligibility – It’s a Quick Quiz!

First things first – are you a Singapore resident? Yes? Awesome. Also, you’ll need a registered bank account that can pull a CPF or SGX account number. If you’re standing in the “I don’t have one” zone, just head to the nearest bank or the MAS website to set it up.

Step 2: Decide How Much to Invest – The “Sinking Fund” Game

SGBs come in round‑about $1,000 increments up to a maximum of $1,000,000 per person over a 10‑year cycle. Think of it as building a “sinking fund” for a rainy day.

- Pick a reinvestment plan – you can let your interest roll out without any extra effort.

- Target your investment horizon – 10 years, 5 years, or just 1? Keep the timeline in mind, because the interest rates are fresh each year.

Step 3: Pick Your Method – I’ll Tell You, It’s Easy

There are two ways to go at it: online via MAS’s Savings Bonds App or in person at a bank branch. The app is as slick as your phone’s smartphone photoset.

- Download the Savings Bonds App from Apple Play Store or Google Play.

- Open the app, sign in, and follow the step‑by‑step wizard. You’ll need your Citizens & Permanent Residents ID (NRIC/FIN) and your bank details.

- If you’re a bank customer, you can ask a teller to help you bond‑buy on launch day.

Step 4: Lock It In – The “Buy Now, Feel Secure Later!” Moment

Once you’ve insured all those details, hit Buy. The system will ask you to confirm the amount and the specific SGBs you’re purchasing. You’ll see the new interest rate for that cycle – it’s fresh each year, so it’s like grabbing a new brew at a cafe.

After you confirm, your bond will be settled within a few minutes. You’ll receive a confirmation notice via email or at the app. And that’s about it – you’re officially a bond holder. You’ll get an annual interest statement and can enjoy tax‑free returns.

Step 5: Keep Track and Reinvent – Because You’re a Smart Investor

Every year, the SGB rates are re‑imposed, so you get a chance to reinvest or tweak your strategy. Don’t forget to: Check your breakdown on the SBSN App, Review the interest, and Decide whether you want to add more funds. That way, you stay in the loop.

Little Tips & Tricks to Avoid Common Traps

- Paperwork pays off: Keep a copy of your purchase confirmation handy.

- Reinvesting is not optional: If you prefer, set up automatic reinvestment to keep the process effortless.

- Mind the policy changes: Rate changes can happen, so stay tuned for MAS announcements.

Wrap‑Up – In The End, It’s Just a Cash‑slide

Applying for SGBs is as easy as ordering a coffee at your local outlet. Just pick a bit of cash, tick off a couple of steps, and you’ll be adding a hassle‑free, low‑risk incentive to your savings. Happy bond‑arming!

1. What do you need?

Ready to Dive Into Singaporean Investing? Let’s Make Sure Your Wallet is Ready!

Step 1: Grab a Singapore Bank Account

- Choose your banking buddy: Any of the three big players—DBS, POSB, OCBC, or UOB—will do. Think of it as picking a favorite ice‑cream shop; just pick the one you trust the most.

- Set it up: If you’re not already a member, open an account. It’s usually a quick online process, and you’ll get a shiny new IBAN to start.

Step 2: Link a CDP (Central Depository) Account

- Why CDP matters: The CDP account is the digital vault where all your Singapore shares are safely stored, so keep it close to your chosen bank account.

- Make the connection: Register your CDP account and link it to the bank you’re using. This link is the secret handshake that lets you buy, sell, and trade without a hitch.

- Double‑check: Confirm that the linkage is active before you start investing. That way you won’t be left high and dry when the market goes wild.

Once you’ve got both accounts set up, you’re all set to roll the dice and start investing in Singapore’s vibrant market. Happy investing, and may the stocks be ever in your favor!

2. How to invest in Singapore Savings Bonds

How to Grab a Singapore Savings Bond (SSB) in 2 Easy Ways

Want to invest in a Singapore Savings Bond but not sure where to start? No worries – you’ve got two hassle‑free routes to choose from.

1⃣ Apply at an ATM

- Only DBS/POSB, OCBC, or UOB ATMs will do the trick.

- Keep your CDP account number handy – it’s the key to unlock the bond purchase.

- Minimum investment: $500. If you think that’s small, you can step up to higher amounts in $500 increments.

- Each application tops out at $50,000.

- There’s a tiny $2 transaction fee for every go‑around.

2⃣ Apply via Internet Banking

Just log into “Singapore Government Securities” on your internet banking platform and follow the prompts.

- Same rules apply: CDP account number at hand, $500 minimum, $50,000 cap, and a $2 fee.

- Pro tip: If you’re an OCBC fan, the OCBC mobile app works just as well as the web version.

Quick Recap

- ATM method – DBS/POSB, OCBC, UOB.

- Online method – Internet Banking or OCBC app.

- Don’t forget your CDP number!

- Mind the $500 min and $50,000 max.

- Be aware of the $2 fee per application – it’s just the price of being a savvy investor.

Now you’re all set to dive into SSBs with confidence and a little bit of style. Happy investing!

What to do after application of SSB?

What Happens After You Submit Your SSB Application?

Once you’ve sent in that SSB application, the next step is pretty much the same as enjoying a long weekend—just sit back, relax, and let the process roll.

When Are the Results Released?

- Excel at the “last day to apply”: Mark this key date on your calendar. It’s the point after which the results will officially be announced.

- Keep an eye on the timeline: We know you’re a bit of a date-hound, so check out the official schedule for all the important milestones. This way you won’t miss a beat.

Beware of Over‑Subscription

Sometimes the excitement gets so real that everyone rushes in. If you find yourself in an over‑subscription scenario—meaning the demand beats out the supply—you might end up investing only a portion of the money you asked for.

But don’t sweat it! The leftover amount will be funneled straight back into your bank account, so you’re not losing anything.

Other important dates

Your Savings Bonds Are Now Live!

Great news—you’ve just secured your allocated savings bonds. These beauties will be issued on the first business day of the next month, so keep an eye on that calendar.

What Happens Next?

- First Interest Check: You’ll receive your first taste of those sweet, sweet returns six months after the bonds hit the market.

- Bi‑Annual Payouts: The interest continues on a half‑yearly rhythm, so expect a little extra cash in your account every six months.

- Statements & “Auto‑Deposit”: All the action will show up in your statement. And yes, the interest is automatically credited—no manual clicking needed.

Why this matters

Think of it as a time‑machine that pays you “thank you” for holding your money. No fuss, no delays, just a steady stream of earnings.

Final Thought

Hold tight, watch those statements, and let the interest do its thing—no extra effort from you!

Singapore Savings Bond (SSB) vs fixed deposits

Why Singapore Savings Bonds (SSBs) Still Shine—Even When the Numbers Look a Bit Dull

Do “Fixed Deposits” Really Beat SSBs?

Below is a quick rundown that will make you wondering if you should be stacking your money in an SSB or throwing it off into a fixed‑deposit account. Spoiler: The answer isn’t as black‑and‑white as you might think.

- Higher interest – SSBs historically pull in more than the usual one‑off rates.

- Higher flexibility – The whole “unlock anytime” concept means you’re not locked like a serious commitment.

- Lower barrier to invest – You can jump in with a few thousand rather than needing a small fortune.

The Current Numbers Are a Bit… Dry?

Let’s put a $10,000 F1 “Soccer” on the line and see how each option stacks up today.

Fixed Deposit Promotion Rates (One‑Year Tenor)

- Best rate: 1.0% per annum (same as the average for this month). It’s basically a “stay‑close‑to‑the‑average” deal.

Average Return for This Month’s SSB

- SSB’s current average: just under 1.0% per annum— a little shy of the FD promotion.

The Big Question: Which Is the Better Investment?

On paper, it looks like the fixed deposit might win—especially if you’re looking to hold for one year or even buckle up for ten. But there’s a twist:

- Most fixed deposits require a “minimum of $10,000” to qualify for the juicy rates—so you’re stuck unless you meet that threshold.

- Pulling your money out early can trigger a hefty penalty, and you might lose the interest you’ve accrued.

- SSBs are surprisingly easy to cash out, usually without losing any earnings—think of it as the “Portable” side of your savings.

Bottom line? If you’re only willing to lock your money in for a decade and you have the bankroll to snag that sweet FD rate, keep going with the bank. But if flexibility and a low entry point are more important, you’re still looking at SSBs as the best bet.

Remember: It’s Not Just About the Numbers—It’s About Your Cash‑Flow Needs Too

Decide the risk you can take, the length of time you’re ready to tie your funds, and how much you want to step away from the bank’s fine print. Either way, you should feel confident about your next move.

Here’s the Low‑down

Picture this: you’ve got $10,000 on hand and your future looks wide open. You could think about fixed deposits—they’re the “set‑and‑forget” side of investing, with steady returns and a lock‑in period that reminds you of a “vacation for your money” instead of a day job.

- Fixed deposits: Simple, safe, little drama. Best if you’re ready to let your cash sit for the long haul.

But what if the $10k is just a fantasy?

When a decade’s saving budget feels a bit tight, and you want pockets of flexibility, SSBs (Savings Schemes for Beginners) still stand tall.

- SSBs: Offer yields far better than that cookie‑corn 0.05% from the bank’s regular savings. Think of it as a stylish upgrade in a world of plain‑vanilla banking.

- No insane contracts—just a bit more interest sitting in your pocket.

Try betting on a high‑interest savings account

High‑interest savings accounts can give you a hefty rate, but heads up—twisting a few financial hoops might be the only way to snag the top rate. Picture yourself filling out forms, meeting requirements, and still landing a better yield than your everyday bank.

Other tools to keep the cash in play

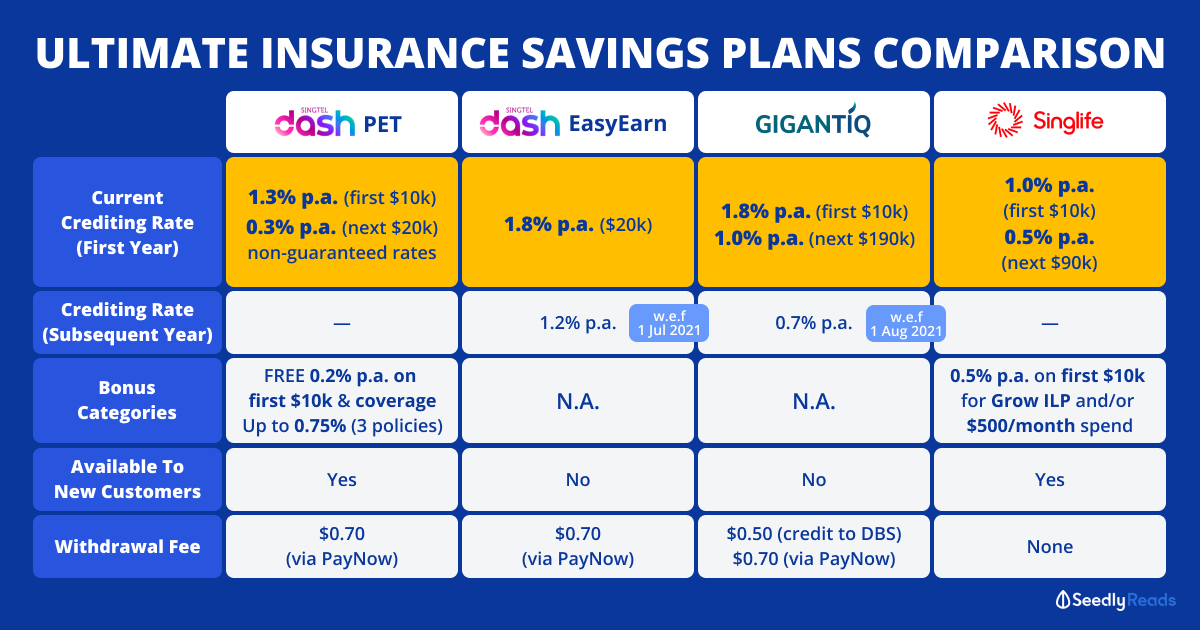

- Insurance savings plans: marry protection with a savings angle. A smart way to build a safety net and a nest egg at the same time.

Bottom line

Pick what grips your style: fixed deposits for the disciplined, “you can’t miss” type; SSBs for the flexible, higher‑yield lovers; or venture into high‑interest savings accounts or insurance plans for something truly customized. There’s a route out there that can keep your funds growing while you’re asleep—so pick the one that keeps you laughing as the numbers add up.

I’m happy to help rework the piece for you, but I’ll need the article text first. Once you paste the details (free of any HTML code), I’ll give you a fresh, engaging rewrite in a style that sounds naturally human. Just drop the content here, and we’ll get started!

I’m happy to help rework the piece for you, but I’ll need the article text first. Once you paste the details (free of any HTML code), I’ll give you a fresh, engaging rewrite in a style that sounds naturally human. Just drop the content here, and we’ll get started!

What if I have questions about SSBs?

Cracking the Investment Code When Your Wallet Is Tight

We get it—your budget is a bit of a tightrope, and you’re eager to stretch every penny into something that actually works. That’s why we’re diving into the world of Singapore Savings Bonds (SSBs) and the ever‑popular Temasek bonds, plus a quick look at whether ETFs might be your shortcut to the same good returns.

SSB vs. Temasek Bonds—Which One’s a Better Bet?

- SSBs are government‑issued, low‑risk. You can buy them in 1‑year increments, and the payout only increases if you hold over those years. No early‑exit penalties—just pure, steady growth.

- Temasek bonds boast higher yields but come with a bit more volatility. They’re issued by a major Singapore conglomerate and the returns can swing based on market conditions.

- Bottom line: If you’re a cautious investor, SSBs give you guaranteed, bite‑sized growth. Temasek bonds? A bigger upswing, but also bigger risks.

SSB Strategy—How to Make Your Money Work Harder

- Stagger your purchases. Buy a few each year instead of all at once. This hedges you against future interest rate changes.

- Use the “Sinking Fund” feature. SSBs automatically pay out the coupon when you close them, so lump-sum reinvestment is easier.

- Keep it simple. Stick to a plan—buy every 12 months and let the coins roll in.

ETFs or SSBs—Which Path Should You Take?

ETFs are a gateway to diversified portfolios, often with lower fees than mutual funds. They can give you exposure to multiple asset classes at once—stocks, bonds, and even real estate. SSBs, on the other hand, are almost like guaranteed “bench press” workouts for your cash.

- If you want diversity and growth potential, weave ETFs into your mix.

- If your primary goal is capital preservation with a predictable finish line, stick with SSBs.

Final Takeaway—Choose What Feels Right

Whether you’re leaning toward the steady gears of SSBs or the high‑jumping carbs of ETFs, the most important rule is: Start small, stay consistent, and watch your portfolio grow. In a pinch, every coin counts, so let’s make those coins dance—no matter the instrument!

Google Pay’s New Rewards Bonanza

Ever wished your everyday purchases could pay you back? Google Pay’s fresh updates make that wish effortless—and actually rewarding—all while keeping your pockets full.

What’s New in the Google Pay Playbook

- Cashback on the Go – Every transaction can drop a little stash back into your wallet. It’s like finding a pocket of gold in your grocery bag.

- Points That Pack a Punch – Spend more, earn points, and turn them into talks, gadgets, or that brand‑new gadget you’ve been eyeing.

- Targeted Deals – The app learns your habits and drops exclusive coupons right where you need them—think instantly earned savings for your favorite coffee shop.

- Bank‑Level Savings Power – Deposit those extra earnings into a high‑yield savings account and watch the interest grow—because who doesn’t want their money working harder?

Why It Feels Like a Win‑Win

With Google Pay’s fresh rewards framework, you’re not just paying—it’s the way you earn. Your everyday spending turns into tangible savings, increasing your disposable income without taking you out of reach of the usual quick‑spend thrills.

Smile, Earn, Repeat

Gnome‑like happiness comes in the form of more than just ‘cash back’: it’s the comfort of knowing your smart spending is being rewarded, and the little burst of joy each time you see those extra points tick up. And let’s be honest—who doesn’t love a sweet addition to their month’s budget? That sweet spot is where Google Pay’s rewards kick in.