The Hilarious Reality of a Lamborghini Crash

Can a Tiny Toyota Driver Crash a Lamborghini Without Going Broke?

Picture this: you’re behind the wheel of a modest Toyota, scrolling through your playlist, when a sudden blow‑to‑the‑right forces your little sedan into a high‑end Lamborghini. The sleek sports car spins, ricochets into the car ahead, and everyone’s eyes go wide. Sound like a nightmare? Not really—if you’ve got the right insurance.

What Happens When the Heavyweight Gets Hit?

- Surprise! Insurance Saves the Day: Singapore’s third‑party liability limit tops out at S$5 million, triple the price of a new Lamborghini (about S$1.5 million). So, theoretically, the policy can cover the entire cost of repairs.

- It’s Not an All‑Out Disaster: The Lambo wasn’t totally wrecked; the damage fits comfortably within the insurance window. That means no “sky‑high” bills.

- Your Share is Minimal: Even if the crash had escalated into a two‑car pile‑up, the driver would only be responsible for the standard excess and a few extra charges—nothing life‑shattering.

Bottom Line – Keep Calm and Get Insured

If you’re cruising in a Toyota (or any car) in Singapore, just make sure your comprehensive insurance policy is up to par. Next time a Lamborghini crosses your path—one way or another—your premium should keep the financial compass steady.

What Happens When You Crash Into a Fancy Car (And Are Still Not the Hero)

Car insurance usually covers the drama of a crash… but not always. Picture this: you’re driving a Toyota under a TPO/TPFT plan and slam into a shiny Lamborghini. You’ll never open your wallet for the other driver’s damages—thanks, coverage! Yet you’ll still have to pay for your own car’s dents and any boo-boos you might have suffered. If the wreck hits the “hospital tier”, those bills can sky‑rocket.

Why the Real Show‑stopper Is the Cause, Not the Car

It turns out the culprit matters more than the price tag. If you’re found to be drinking and driving or you dodge reporting the incident within 24 hours, your insurer pulls its mumbo‑jumbo and refuses to cover any of the bad guy’s damages. In that situation, you could wind up swinging for the fences — literally — owing tens, even hundreds, of thousands of dollars to the Lamborghini owner for repairs and medical bills. The money might even surpass what the average Singaporean earns in a year (remember that S$66,645‑plus cost to fix a Lamborghini transmission!).

Does the Luxury Car Make the Damage Worse?

We’re spelling it out in plain English: no. In Singapore, most drivers have comprehensive coverage, so crashing into a Lamborghini doesn’t automatically mean you’ll pay more than a crash into a midsize sedan. The fancy car doesn’t magically inflate your liability.

Short‑Term Price Tags

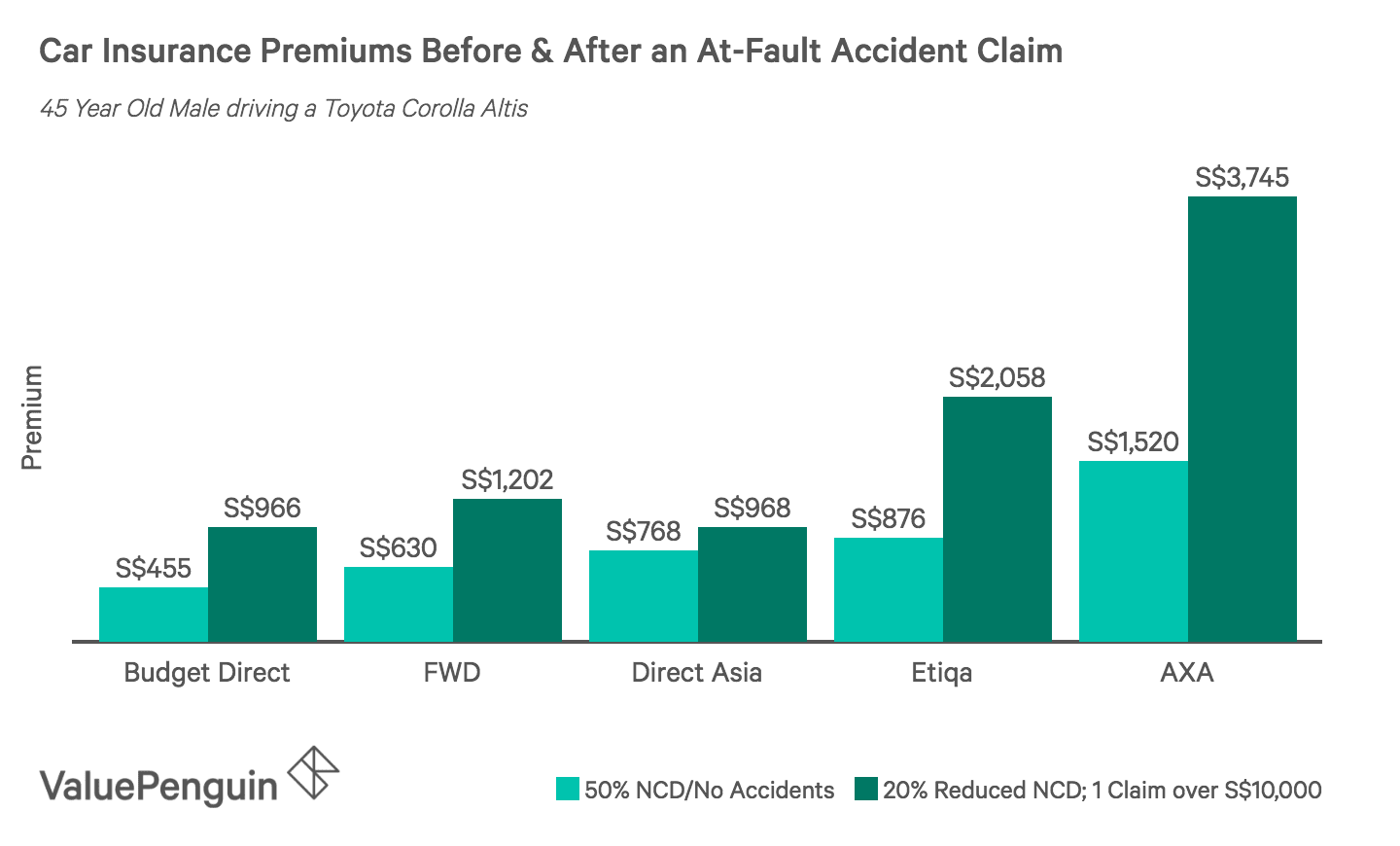

- Insurance Hike – Your premium can double after a claim because a no‑claims‑discount (NCD) slumps by 30% and the claim history turns up.

- Legal Fees – If the other driver sues, you might hit up to S$3,000 in legal coverage, but that’s not guaranteed.

Long‑Term Aftermath

A crash that lands you in the blame column ripples through your budget for months—or even years—regardless of whether the other vehicle was a Toyota Camry or a Lamborghini Aventador. The only time that a super‑expensive car changes the equation is if the value tops the USD 5 million mark and the other side can’t recover through insurance.

Bottom Line

So, keep your wheels on the straight road, report any incident ASAP, and avoid that tempting sip of beer before you drive. Trust me, your head—and your bank account—will thank you.