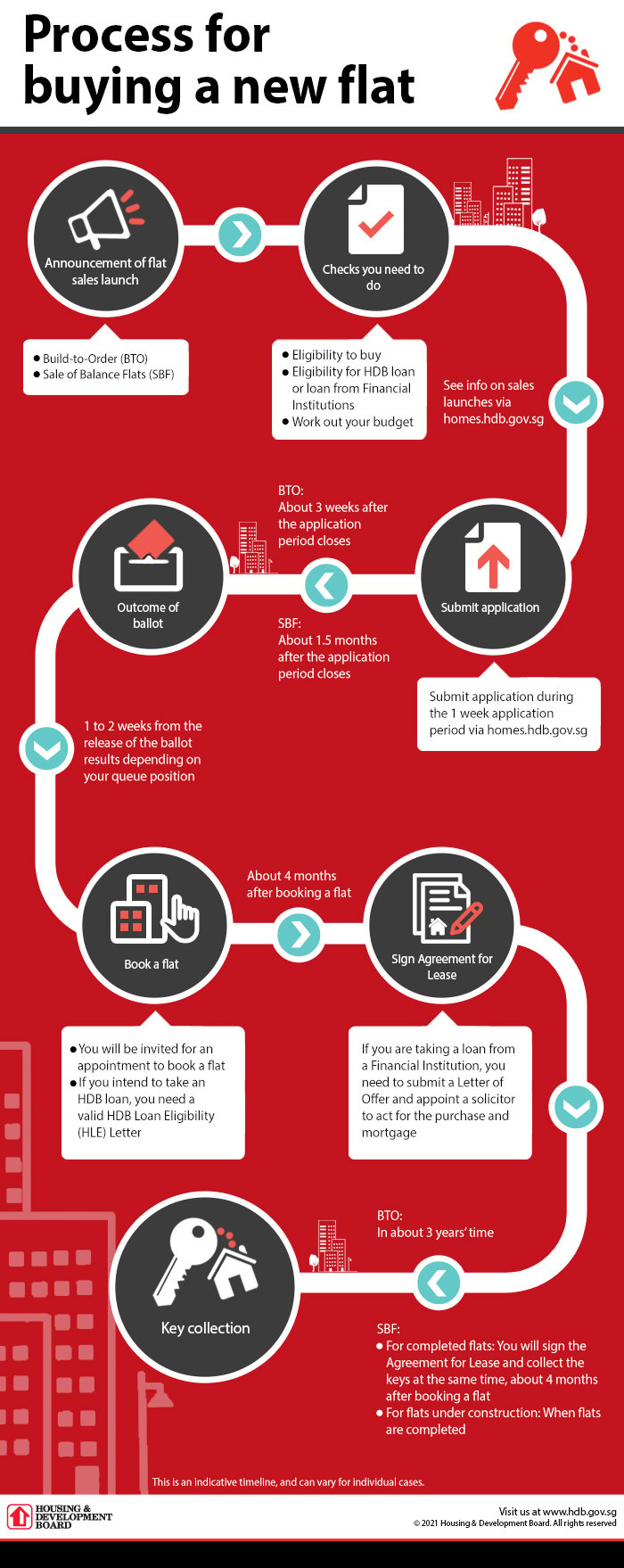

BTO Home Buying in Singapore: A Cute (and Slightly Scary) Adventure

Imagine you’re a newly minted couple, scrolling through the endless sea of flats, when you stumble upon that sweet “Build‑to‑Order” bazooka. Owning a BTO flat is practically mandatory for Singapore dreamers—yes, you’ve got the “romantic” vibe of a warm hug from the Ministry of Housing. But behind every heart‑warming headline lies one rock‑solid truth: the payment timeline.

Why the BTO Payment Curve is Not Your Average Roller Coaster

The excitement of finally calling a place “home” can be deceiving. If you’re not careful, the payment schedule will feel like a cliff‑hanger episode you can’t afford to miss. The trick is to arm yourself with a solid financial plan before you hit the “Apply” button. Here’s why that matters:

- Cash Flow Confidence: Having a clear picture of how much you can shove into each payment milestone keeps the anxiety at bay.

- No Surprises, Just Sirens: Knowing when the payments come helps you steer away from last‑minute panic.

- Future‑Proofing: You’ll avoid that dreaded “I didn’t budget for this!” moment when the date arrives.

Our Golden Rule for BTO Aspirants

Before you send that eager email, take a step back and ask yourself: “Do I have my money in order?” If the answer’s a few bumps in the road, re‑check your finances. Align your savings, loans, and budget—only then should you jump into the BTO maze. Because the true joy of home ownership isn’t just buying a place—it’s actually paying for it without a single bad‑guy episode.

Final Thought

Picture a tiny kitchen where you’ll cook dinner for your future kids, or a cozy living room where you’ll watch your favorite show—yes, you’re buying a home. Make sure the payment plan is the sturdy foundation that holds that dream together.

BTO Payment Timeline Cheat‑Sheet

Grab a coffee and sit tight — we’ve turned the whole BTO payment maze into a slick, step‑by‑step guide so you’ll know exactly where you stand every time you put your signature on the dotted line.

The Quick‑Start Steps

- Initial Deposit (usually 5%) – the first payment you toss over the counter to lock in your new flat.

- Second Payment – a bit later, you’ll be asked for that next chunk, often around 20%.

- Third Payment – get ready for a sizable installment, usually 30%, coming in a few months before the handover.

- Final Payment (balance) – the last dash, covering the remaining 35%, due right before your keys are handed out.

Every payment level is tied to a milestone in the build‑to‑order process, and our cheat sheet has the dates, percentages, and a few quiet reminders to stay on track.

Need a Quick Cheat?

Print this out, paste it into your phone, or just keep the PDF handy in your wallet. With this cheat sheet, you’ll never miss a payment deadline or find yourself staring at a blank bank statement after signing away your future home. Happy building!

HDB BTO payment timeline

Buying a Brand-New Home – Your Step‑by‑Step Money Guide

1⃣ Stage of Purchase: “BTO” (Built‑To‑Order) or “Flat Booking”

- BTO Application – Drop in a modest $10 application fee. Pay via a credit card or any of the popular mobile payment apps like DBS PayLah!, UOB Mighty, OCBC Pay Anyone – we’re practically digital pirates here!

- Flat Booking – Think of this as “option fee” that sits snugly in your down‑payment pile.

- Two‑room Flexi: $500

- Three‑room: $1,000

- Four‑room and bigger: $2,000

Pay using NETS – the card of the future!

2⃣ Signing the Agreement for Lease

- Stamp Duty – It’s a breakdown that looks almost like an Excel sheet:

- First $180,000: 1% – that’s about $1,800.

- Next $180,000: 2% – $3,600.

- Next $640,000: 3% – $19,200.

- Remaining: 4% – yep, it keeps climbing.

Grab your Cashier’s Order and CPF for that.

- Conveyancing Fees – These are tiered. Picture a sliding scale, but with numbers:

- First $30,000: $0.90 per $1,000 → $27.

- Next $30,000: $0.72 per $1,000 → $21.60.

- Remaining amount: $0.60 per $1,000 → we’ll crunch that later.

3⃣ Down‑Payment: The Big Bucks

- If you’re pulling an HDB loan, you’ll shell out 10% of the purchase price. Easy peasy.

- Bank loan with LTV 75%:

- Cash part: 5%

- CPF &/or #BIG# Cash: 15%

- Bank loan with LTV 55%:

- Cash part: 10%

- CPF &/or #BIG# Cash: 10%

4⃣ Key Collection and Final Fees

- Registration Fee – Two separate escrow fees:

- Lease In‑Escrow: $38.30

- Mortgage In‑Escrow: $38.30

- Survey Fee – Because a house isn’t just a nest. It’s a survey map!

- One‑room: $150

- Two‑room: $150

- Three‑room: $212.50

- Four‑room: $275

- Five‑room: $325

- Executive: $375

- Stamp Duty for Deed of Assignment – It’s just a fraction: 0.4% of the loan amount, capping at $500.

- Home Protection Scheme – If you’re using CPF for loan installments, it depends on your outstanding loan. Don’t worry, the bank calculates that for you!

- Fire Insurance – If you’re on an HDB loan, you’ll pay between $1.62 and $8.10 for five years. Think of it as covering the inevitable “Oh no, a fire!” moments.

5⃣ Balance of the Purchase Price

- Bank loan with LTV 75% – Just 5% of the purchase price with CPF and/or cash to keep the balance tidy.

- Bank loan with LTV 55% – A bigger chunk: 25% of the purchase price with CPF and/or cash. Hefty, but it’s what you pay when you’re buying that bigger house.

There you have it – the full money timetable for your Singapore home journey. It may feel like a buffet of fees, but once you know what’s on the plate, you’re ready to glide through the purchase like a pro. Good luck and may your new home be filled with laughter, love, and plenty of coffee (or your preferred beverage)!

Here’s an illustration for taking an HDB loan

The New‑Home Journey of Mark & Sophie

Singaporeers in their 20s, freshly tied by marriage and ready to make a splash in the property market.

The Game Plan

Mark and Sophie are first‑time buyers with a combined monthly income of $5,000.

They’re eyeing a three‑room BTO flat priced at $300,000.

They’ll use the Staggered Down‑payment Scheme (SDS) and grab an HDB loan that covers up to 90 % of the price for a 25‑year stretch.

Loan repayments will be nailed down using their CPF savings.

The Cash Breakdown

Below is a clean, no‑frills list of all the fees and amounts involved. Think of it as a quick checklist—each item a tiny dollar‑battle worth fighting for.

| What You Pay | How Much |

|---|---|

| Application fee | $10 |

| Option fee (part of the down‑payment) | $1,000 |

| Stamp duty | $4,200 |

| Conveyancing fee | $206.08 (incl. GST) |

| Down‑payment minus option fee | $14,000 (5 % of the price, cash or CPF) |

| Registration fee | Lease In‑Escrow: $38.30 |

| Mortgage In‑Escrow | $38.30 |

| Survey fee | $212.50 |

| Stamp duty for Deed of Assignment | $500 |

| Home Protection Scheme | $132.30 per annum |

| Fire insurance | $4.87 for a five‑year term |

| Balance of the purchase price | $270,000 (HDB loan) |

| Total Costs (including loan) | $305,342.35 |

Quick Highlights

Bottom Line

Mark and Sophie have mapped out a charter that’s both realistic and financially viable.

With a modest monthly income of $5,000, they strategically balance a 5 % down‑payment and a sizeable HDB loan to secure a home that captures the sweet spot of affordability and equity growth.

Takeaway: When you get your numbers straight and use the right schemes, a dream home can be more than just a bedtime story—it becomes a calculable, achievable reality.

If you’re taking a bank loan for your BTO

Crunching the Numbers: How the Bank Loan Breaks Down

Picture this: you’re eyeing a brand‑new home, your first ever loan, and you’re aiming for a 30‑year tenure. Let’s walk through what your wallet will see once you lock in that maximum 75 % loan allowance.

The Ledger You’ll Use

- Application fee: $10

- Option fee (counted toward the down‑payment): $1,000

- Stamp duty: $4,200

- Legal fees (because you need that lawyer the bank rings for you, charge $2,500): $2,500

- Down‑payment minus option fee: 10 % of the purchase price less the option fee, equaling $29,000 (that’s $14,500 in cash + $14,500 in CPF or other cash).

- Registration fee – Lease In‑Escrow: $38.30

- Registration fee – Mortgage In‑Escrow: $38.30

- Survey fee: $212.50

- Stamp duty for Deed of Assignment: $500

- Home Protection Scheme: $120.38 per year (you’ll pay this annually).

- Balance of the purchase price: 15 % of the purchase price (you cover this with cash or CPF). That’s $45,000.

- HDB loan (70 % of the purchase price, subject to 75 % of the full price): $225,000

Totals Galore

Combine all those pieces and the grand total lands at a pretty hefty $307,619.48. It’s the sum of the loan amount, interest due over 30 years, and every fee you’ll face along the way.

Reality Check—What This Means For You

- If the purchase price is $300,000, you’re looking at borrowing about $225,000 (75 % of the price, capped at 70 % for HDB). That leaves $75,000 for you to cover the rest.

- Every month, the loan will eat a slice of your income. Factor in interest, mortgage repay, and the yearly Home Protection Scheme, and you’re in for a marathon—not a sprint.

- That $2,500 in legal fees? Yeah, you’ll pay it up front but it might save you headaches later (no lawsuits about “didn’t we agree on that?!”).

- Stamp duties and registration fees are one‑off costs that can add up quickly. Think of them as the universe’s way of saying, “Here’s your house paid for, but you’ve got to pay the rules.”

- Don’t forget the option fee; that $1,000 has double duty—part of your down‑payment and a stand‑in for part of your cash pocket.

Bottom Line: Is It Worth It?

With the numbers in view, the decision depends on how comfortable you feel with a 30‑year commitment, the projected interest rates, and whether the emotional payoff of homeownership outweighs the financial weight. If you’re ready to dive into this jungle, being transparent about every cost—and staying on top of your repayments—will keep your house dream from turning into a nightmare. Happy house hunting!

Frequently asked questions

What’s the downpayment for BTO?

How the Downpayment Works for Your HDB or Bank Loan

When you’re planning to buy a BTO flat, the amount you need to drop down upfront depends on the type of loan you choose.

HDB Loan

- Downpayment: 10 % of the purchase price

- Why it matters: It’s the easiest way to get your feet on the property—just a tenth of the total cost.

Bank Loan

- Downpayment: 25 % of the purchase price

- What to expect: A higher upfront cost but sometimes you get more flexible interest rates compared to the HDB loan.

So, if you’re leaning toward a bank loan, make sure you’re ready to put down a quarter of the price. If the HDB loan feels more within your reach, a tenth might be all you need.

How long does a BTO project take to complete?

Hang Tight! It’s a Long Road Ahead

Answering the question “How long until we’re there?” usually lands between three to four years. But if you’re dealing with the real world’s twists, the timeline can stretch out to five years.

Why the Extra Time? | The Sneaky Factors

- Supply Crunches – Materials that would normally roll off the line are sometimes in the same short supply as your favorite snack.

- Manpower Shortage – The workforce shortfall means fewer hands to get the job done on schedule.

- Delays – Any hiccup, from weather to paperwork, can add a few extra months to the project.

Picture your coffee turning into a fossil while you wait; that’s pretty close to the reality. Don’t get discouraged—just grab a good book and keep your optimism alive!

How many times can you apply for BTO?

BTO Buying Rules 101

If you’re eyeing a Build‑to‑Order (BTO) flat, here’s the quick‑fire rulebook:

- You must not have already purchased a brand‑new HDB (Public Housing Board), a DBSS (Designated Buy‑Sell Scheme), or an EC (Executive Condominium)

- You also cannot have claimed a CPF Housing Grant before. If you’ve done that, you’re out of the BTO game.

- If you meet both of those conditions, you’re good to go for buying a BTO flat—up to two times.

Why the Double‑Buy Limitation?

Basically, the government wants to keep the market fair and avoid everyone lining up for the same bunch of units. Two chances save the gravy for a broader crowd.

Need a Top‑Hint?

Check out Temporary Occupation Permits (TOPs)—they’re the special pass that let you sit in your new apartment before you officially move in. The details? Tucked inside the 99.co original piece.

Wrap‑Up

So, use the hoops we sprinkled: no previous new‑property purchase, no earlier CPF grant, and you’re set—two tries to secure that BTO sweet spot. Happy hunting!